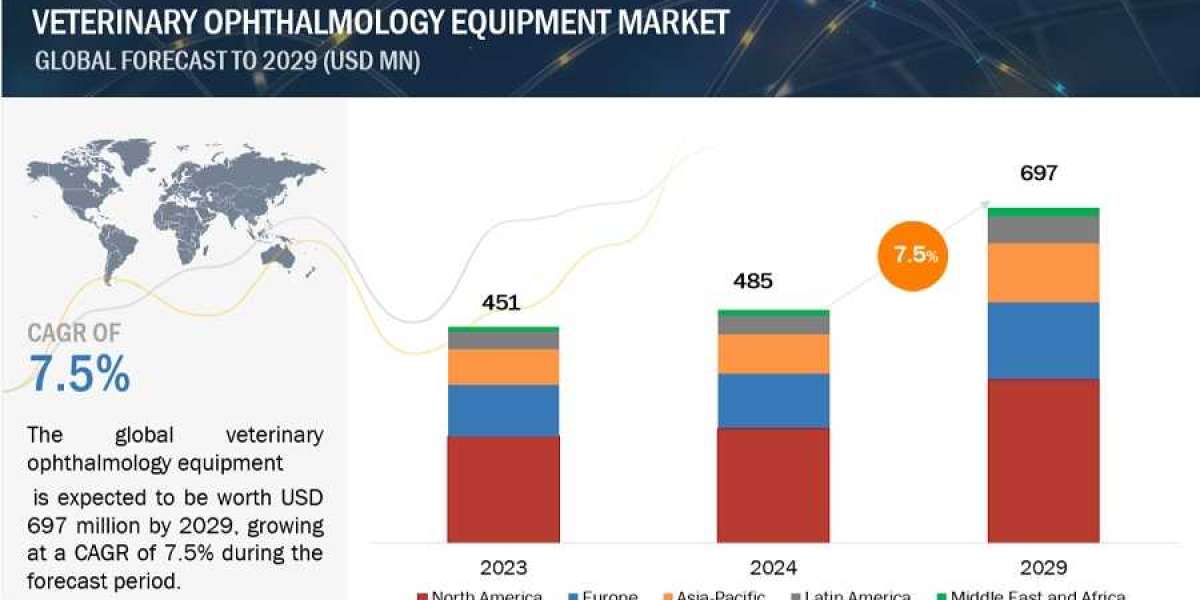

The size of global veterinary ophthalmology equipment market in terms of revenue was estimated to be worth $485 million in 2024 and is poised to reach $697 million by 2029, growing at a CAGR of 7.5% from 2024 to 2029.

The Veterinary Ophthalmology Equipment Market is fueled by increasing demand for specialized pet eye care, technological advancements, and increased pet healthcare expenditure, but challenges include high costs and limited specialist access.

In this report, the veterinary ophthalmology equipment is segmented into – animal type, application, product, end user and region.

Key Market Players:

The key players in the market include Bausch + Lomb Corporation (Canada), Revenio Group Oyj (Finland), Halma Plc (Keeler, a wholly owned subsidiary of Halma Plc) (UK), Baxter International, Inc. (Hill-Rom, a wholly owned subsidiary of Baxter International, Inc.) (US), AMETEK, Inc. (Reichert, Inc., a wholly owned subsidiary of AMETEK, Inc.)(US), HEINE Optotechnik GmbH Co. KG (Germany), LKC Technologies, Inc. (US), IRIDEX Corporation (US), Optomed Plc (Finland), Ocularvision, Inc. (US), AN-VISION (Germany), Eidolon Optical LLC (US), Yuesen Med (China), Ocuscience (US), GerVetUSA (US), Kowa American Corporation (US), AJL Ophthalmology S.A. (Spain), Optibrand Ltd. (US), Alcon Inc. (Switzerland), USIOL, Inc. (US), I-MED Animal Health (Canada), Freedom Ophthalmic Pvt. Ltd. (France), New World Medical (US), Nova Eye Medical (Australia) and CorNeat Vision (Israel).

Download the PDF Brochure at https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=186056447

Veterinary Ophthalmology Equipment Ecosystem

In the veterinary ophthalmology equipment market, the ecosystem encompasses a network of interconnected stakeholders and components, ranging from manufacturers and distributors of ophthalmic devices to veterinary clinics, hospitals, and research institutions. Manufacturers develop and supply a diverse range of equipment, including fundus cameras, optical coherence tomography (OCT) scanners, surgical instruments, and diagnostic tools tailored specifically for veterinary ophthalmology.

Distributors play a crucial role in the supply chain, ensuring the efficient distribution of equipment to veterinary facilities worldwide. Veterinary clinics and hospitals serve as end users, employing ophthalmic equipment for routine eye examinations, diagnostics, and surgical interventions in animals. Regulatory bodies and industry associations also influence the market landscape by establishing standards, guidelines, and certifications to ensure product quality, safety, and compliance. Overall, this interconnected ecosystem fosters collaboration, innovation, and advancement in veterinary ophthalmology, ultimately benefiting both animal patients and care givers.

By product, Surgical Equipment, Disposables, and Implants are expected to show the highest CAGR from 2024 to 2029.

The product segment is segmented into diagnostic devices and Surgical Equipment, Disposables, and Implants. The rising demand for veterinary ophthalmic surgeries, coupled with the higher cost and frequent replacement needs of surgical equipment, disposables, and implants, contributes to this segment experiencing the highest CAGR in the veterinary ophthalmology equipment market.

By application, treatment is expected to show the second highest CAGR from 2024 to 2029.

The combination of increasing prevalence of eye disorders, advancements in treatment technologies, growing demand for minimally invasive procedures, pet owner awareness, expansion of specialty clinics, increased healthcare spending, and technological innovations collectively contribute to the high growth rate of the treatment segment in the veterinary ophthalmology equipment market.

By animal type, canine is expected to grow at the largest share of the global veterinary ophthalmology equipment market.

Pet owners are increasingly aware of the importance of regular eye examinations and treatment for their canine companions. Advances in veterinary medicine have expanded the range of available treatment options for canine ophthalmic conditions, including surgical procedures, pharmacological treatments, and advanced diagnostic techniques. The larger dog population, breed predispositions to certain eye conditions, higher pet healthcare spending on dogs, and availability of specialized equipment solidify the canine segment's position as the leader in the veterinary ophthalmology equipment market.

Direct Purchase at https://www.marketsandmarkets.com/Purchase/purchase_reportNew.asp?id=186056447

North America accounted for the largest share of the global veterinary ophthalmology equipment, by region in the forecast period.

North America holds the largest market share in the veterinary ophthalmology equipment market due to factors such as high pet ownership, advanced veterinary infrastructure, pet health awareness, key market players, and a favorable regulatory landscape. Pet owners are more likely to seek veterinary attention for their pets' eye problems, leading to a larger market for ophthalmic equipment. However, developing veterinary infrastructure and lower disposable income levels in other regions may limit the market size. Despite these challenges, North America's high pet ownership rate, emphasis on pet healthcare spending, advanced veterinary infrastructure, and key market players contribute to its market dominance.